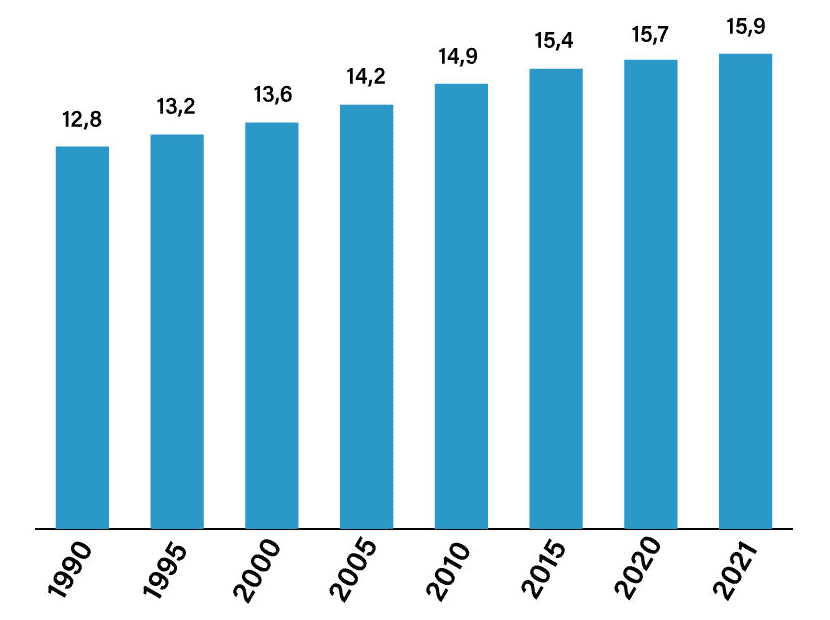

Clear the way for a new financing system

To ensure that health insurance remains efficient and affordable in the future - especially in view of demographic developments and medical and technological progress - we need far-reaching and sustainable structural reforms that address both the financing and the benefits side. On the financing side, income-independent health care premiums are the best way to achieve this. On the benefits side, the most important thing is to intensify competition and to concentrate the catalogue of tasks on basic security.

The central reform step must be the complete decoupling of the financing of health care costs from the employment relationship. The best way to achieve this is to switch financing to income-independent health premiums with payment of the employer's share in gross wages and tax-financed social compensation for those on low incomes. In such a health premium model, neither wage and salary increases nor premium increases can lead to higher additional personnel costs. Social equalization can be organized more precisely and transparently through the tax and transfer system than through the statutory health insurance system. The necessary redistribution volume can thus be reduced. Today's wage-based contributions act like a punitive tax on labour.

©AdobeStock F

Strengthening competition and increasing personal responsibility

Demand-oriented, quality-assuring and cost-effective structures and services in the health care system require competition-oriented control processes and room for manoeuvre for all market participants. The expansion of competitive elements is one of the most effective means of limiting the development of expenditure, in particular to avoid inefficiencies in the provision of services and in organisational structures as well as disincentives for insured persons and service providers. Therefore, more contractual freedom for the health insurance funds in negotiating prices, quantities and qualities with the service providers - in compliance with antitrust and competition law regulations - as well as greater scope for the health insurance funds in offering different forms of care to the insured are required as a matter of priority.

A state-organised health care system financed by compulsory contributions can only remain efficient and financially viable if it is limited to a basic level of security. The aim should be to ensure that, as a matter of principle, only those services that are necessary, evidence-based and economically viable are financed. In addition, deductibles provide incentives for health-conscious and cost-conscious behaviour on the part of the insured and take account of the principle that, in accordance with the principle of subsidiarity, a social insurance system should only provide benefits that the individual cannot pay for himself. In this context, upper limits on burdens prevent individuals from being overburdened. A state-organised health care system financed by compulsory contributions can only remain efficient and financially viable if it is limited to basic coverage. The aim should be to ensure that, as a matter of principle, only those services that are necessary, evidence-based and economically viable are financed. In addition, deductibles provide incentives for health-conscious and cost-conscious behaviour on the part of the insured and take account of the principle that, in accordance with the principle of subsidiarity, a social insurance system should only provide benefits that the individual cannot pay for himself. Upper limits on the burden prevent individuals from being overburdened.