Structural reforms strengthen performance and competitiveness

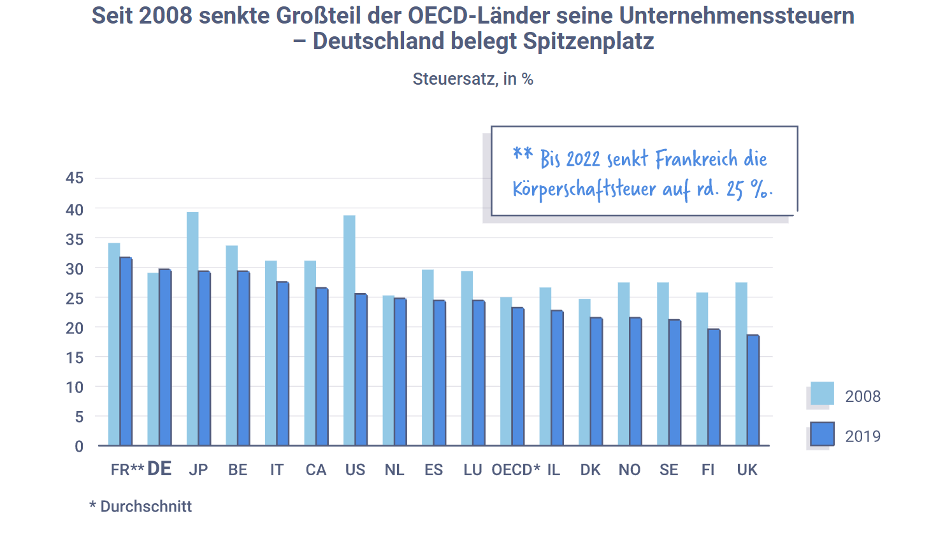

An internationally competitive tax system is a must for every government. Now that Germany has become a high-tax country for companies, it needs competitive tax rates. Additional financial or bureaucratic burdens, on the other hand, would be misguided. A modern tax system contributes significantly to the economic recovery after the Corona crisis and promotes innovation and employment in the long term.

Photo: AdobeStock everythingpossible

Addressing tax reform - promoting growth, jobs and investment

Fairness in performance as a yardstick for tax policy

Modernise tax procedural law in a practical way

Refrain from the misguided path of new or higher taxes

Facts and figures

Information on the electronic wage tax card

The procedure of electronic wage tax deduction characteristics (ELStAM) has replaced the former wage tax card. After registering their employees, employers receive the taxation characteristics (e.g. tax class, religious affiliation, factor) relevant for the wage tax deduction electronically from the tax authorities.

The applicable provisions on the electronic procedure are set out in the application letter of the Federal Ministry of Finance dated 8 November 2018 ("Elektronische Lohnsteuerabzugsmerkmale (ELStAM); Lohnsteuerabzug im Verfahren der elektronischen Lohnsteuerabzugsmerkmale"). Further information can also be found at Website of the tax authorities website. In addition to current procedural information, a list of the most frequently asked questions and answers regarding the ELStAM procedure is also available here.

The BDA is committed to continuously improving the ELStAM procedure and developing it further in the interest of business practice. On the initiative of the BDA, an employer newsletter has been set up by the tax authorities to inform companies about innovations and problems in the ELStAM procedure. Registration for the newsletter takes place via the Elster portal of the tax authorities.