Reduce bureaucracy in payroll accounting

If employers take on social insurance tasks, then this must and can only necessarily mean that the tasks can be fulfilled without costly bureaucracy. But that is not the case today. The thicket of social security regulations is accompanied by considerable liability risks and causes enormous administrative costs for companies. Problems are caused in particular by the complicated calculation of social security contributions, the escalating reporting and certification system, and the differences between social security and tax law.

©AdobeStock Jirapong

In a study - Bureaucratic costs and new ways to avoid bureaucracy by the vbw - it was found that if the time needed to fulfil requirements of sovereign regulations increases by 1%, GDP decreases by 0.03% on average. If the time needed to fulfil the requirements of sovereign regulations were to fall by 10%, this could be accompanied by an increase in GDP of 0.3%, which would mean an increase of around €9.1 billion. (Source: vbw 2017)

Our proposals to simplify the law on contributions and registration include the following:

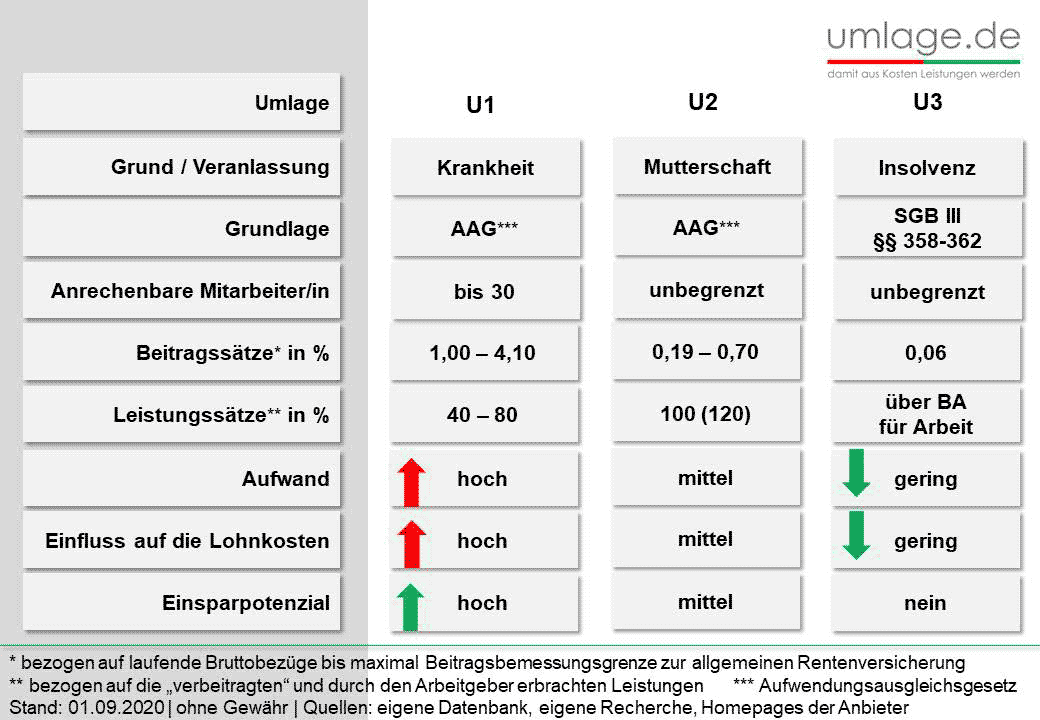

Reduce bureaucracy in the pay-as-you-go system and abolish it in the medium term.

The pay-as-you-go schemes serve to compensate the employer's expenses for continued payment of wages in the event of the employee's incapacity for work, the financial burdens arising from the employer's maternity protection and continued payment of wages in the event of the employer's insolvency by the respective health insurance fund of the employee. The pay-as-you-go schemes are financed by a corresponding employer contribution. The largest cost factor is the U1 procedure of small companies (employers with up to 30 employees). The individual employer must carry out the pay-as-you-go procedure with each health insurance fund with which one of his employees is insured. Accordingly, depending on the statutes of the health insurance fund, different reimbursement rates (currently over 100) and thus also different apportionment rates must be used as a basis and taken into account by the employer.

The most effective reduction in bureaucracy would be achieved by removing the obligation to participate in the pay-as-you-go system. This is especially true since the financing of maternity care during maternity leave is a task for society as a whole (Article 6 (4) of the Basic Law) and must therefore be borne by the general public. However, even if the procedure is retained, a significant reduction in bureaucracy can be achieved by enabling employers to choose a health insurance fund with which to carry out the pay-as-you-go procedure. Companies would thus have a single point of contact for all settlement cases, uniform contribution and reimbursement rates, and uniform reimbursement rules.

At least simplify the artists' social security contribution procedure

Germany is the only country in Europe to have a special social security system for artists. The obligation of companies to pay contributions in accordance with the Artists' Social Insurance Act (KSVG), which was created to finance this system, burdens them with a considerable amount of bureaucracy - above and beyond the cost burden of the artists' social insurance contribution itself. The numerous vaguenesses of the legal regulations and the extensive recording, documentation and reporting obligations in particular contribute to the bureaucratic burden.

The bureaucratic costs of levying the KSK are disproportionate to the income, the Federation of Hessian Business Associations (vhu) has now criticised in a position paper. The KSK collected 260 million euros in levies in 2014. According to the vhu, almost as many costs were incurred in the companies for determining and paying the levies. As evidence, the vhu refers to a study by the Cologne Institute for the German Economy (IW) from 2008, which had already prompted the BDA to issue a position paper against the KSK in 2009. It came to the conclusion that for every euro of levy collected, 78 cents of bureaucracy costs were incurred.(Source: VGSD 2016).

With the law to stabilise the artists' social security levy rate, the disproportion between the levy and the associated bureaucracy was once again dramatically exacerbated. The law introduced extensive monitoring of the payment of the artists' social security levy during audits of employers by the German Pension Insurance Fund. This creates further costs for both the pension insurance institutions and the employers, without changing the amount of the levy to be paid. Such a glaring disproportion between costs and benefits demonstrates the urgency of bringing about simplifications without delay.